2025-11-24 · 2668 words · 13 min

💳 Bybit Card Review 2026 — 6 Cashback Tiers Up to 10%, 100% Back on Netflix/Spotify/ChatGPT/Prime/TradingView

Hands-on Bybit Card review 2026 with actual screenshots — 6-tier cashback structure (Base 2% to Infinite 10%), 100% cashback on Netflix/Spotify/ChatGPT/Prime/TradingView subscriptions, full fees and spending limits by region, real transaction examples.

⚡ Quick answer — should you apply?

If you live in a supported region (EU, Australia, Asia Pacific, Argentina, Brazil, Mexico, Georgia, Kazakhstan, AIFC) and either already trade on Bybit OR you spend regularly on Netflix, Spotify, ChatGPT, Amazon Prime, or TradingView — yes, Bybit Card is worth setting up. The 100% cashback on those five subscriptions alone covers most retail use cases inside the monthly cap, and the 2-4% baseline cashback on regular spending is competitive against major bank cards.

If you're a US person — geo-restricted, skip. If you live in Argentina specifically, run the FX math first (7% + 5% padding may make P2P-and-spend cheaper than the card).

💳 Apply for Bybit Card via my partner link

⚠️ Disclosure: this article contains an affiliate link to Bybit. If you sign up through it, I may earn a commission at no extra cost to you. Bybit is responsible for its own product, terms, and security claims — verify everything on Bybit's official Card page before applying. Educational content, not financial advice.

🩸 Why crypto cards in 2026 — and where Bybit Card lands?

The "spend your crypto" category went from novelty to genuine retail infrastructure between 2024 and 2026. Crypto.com, Coinbase, Bybit, OKX, Binance — each shipped their own card product. Most of them are functionally similar at the surface: tap your phone at a terminal, crypto converts to fiat, payment goes through.

Where Bybit Card differentiates is the 6-tier cashback structure with a meaningful top end (10% on Tier 6 Infinite) plus a focused 100% cashback program on 5 specific subscriptions that most retail users already pay for monthly. The combination is unusually generous if you fit the profile — and rapidly underwhelming if you don't (more on this below).

The card itself is a clean Mastercard, virtual by default with optional physical delivery (~30 days). Visually it's a premium-looking metallic gradient, available in white or dark depending on tier. The physical card is a regular Mastercard at any merchant — there's nothing crypto-branded that draws attention at the terminal.

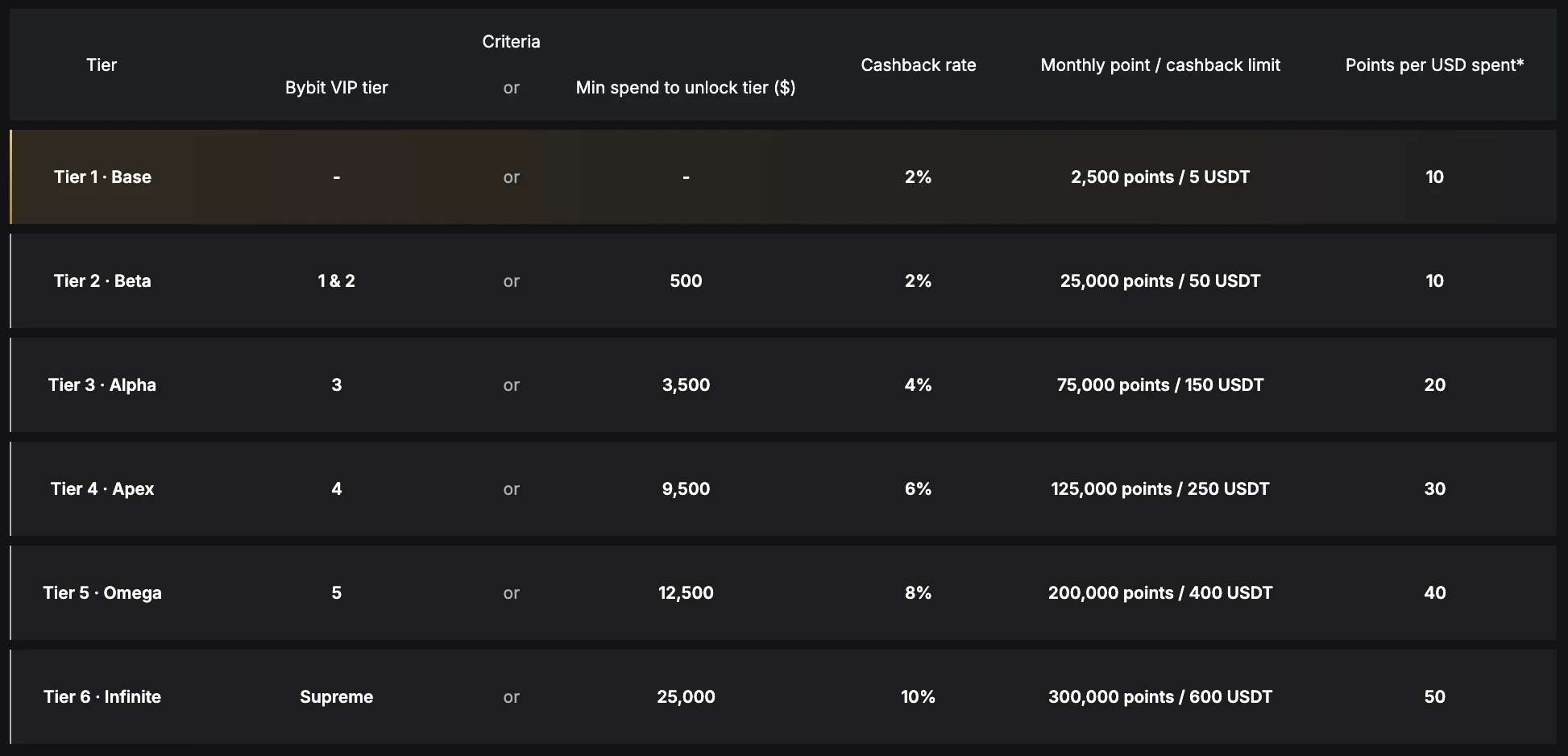

📊 The 6-tier cashback structure — what's actually achievable

This is where most card reviews oversimplify. Bybit Card doesn't have one cashback rate — it has six tiers, each with a different rate and monthly cap. The criteria to unlock each tier is either a Bybit VIP trading tier or a minimum monthly card spend:

Full breakdown of the 6 tiers:

| Tier | Bybit VIP | Min spend ($/mo) | Cashback | Monthly cap | Points / USD |

|---|---|---|---|---|---|

| Tier 1 Base | — | — | 2% | 5 USDT | 10 |

| Tier 2 Beta | VIP 1 or 2 | $500 | 2% | 50 USDT | 10 |

| Tier 3 Alpha | VIP 3 | $3,500 | 4% | 150 USDT | 20 |

| Tier 4 Apex | VIP 4 | $9,500 | 6% | 250 USDT | 30 |

| Tier 5 Omega | VIP 5 | $12,500 | 8% | 400 USDT | 40 |

| Tier 6 Infinite | Supreme | $25,000 | 10% | 600 USDT | 50 |

What this actually means in practice:

- For a typical retail user (under $500/month card spend, no active trading) — Tier 1 Base, 2% cashback, max 5 USDT per month back. That's $60/year on $3K annual spend.

- For a moderate user ($500-$3,500/month spend or VIP 1-2) — Tier 2 Beta, still 2% but cap rises to 50 USDT.

- For active Bybit traders (VIP 3) — Tier 3 Alpha at 4%, materially better.

- For high spenders ($9,500+/month) — Tier 4-5 at 6-8%.

- For the headline 10% — you need Bybit VIP Supreme (extreme trading volume) or $25K/month card spend. This is a marketing top-end, not a realistic target for most users.

Practical recommendation: size the value of the card around 2-4% cashback, not the 10% headline. If you're spending $1,500/month on the card, expect $30-60/month in cashback at base/alpha tiers.

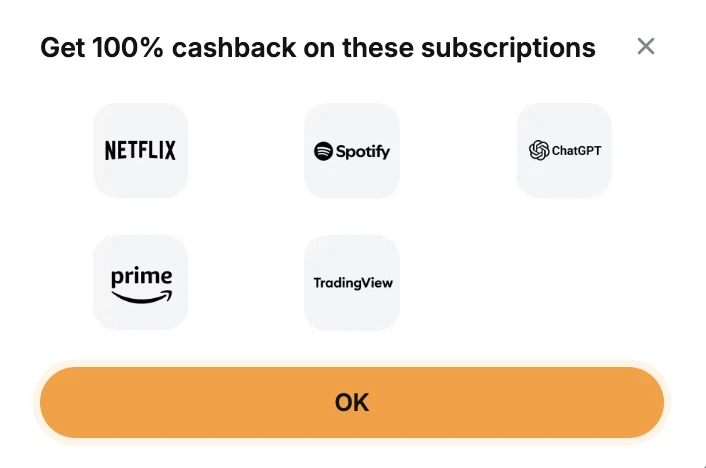

🎬 100% cashback on 5 specific subscriptions — the actual unique value

Bybit ships 100% cashback on 5 specific subscriptions:

- Netflix

- Spotify

- ChatGPT (OpenAI)

- Amazon Prime

- TradingView

If you already pay for any of these, the math is straightforward: pay through Bybit Card, get 100% back as USDT within tier cap. For most users spending $30-80/month on subscriptions across the list, the cap (5-600 USDT depending on tier) covers everything.

This is the actual unique value — most other crypto cards offer 1-2% on subscriptions, not 100%. The list is narrow (5 services) but they're the right 5 for retail users. TradingView Pro at $14.95/month + Spotify $11/month + Netflix $15.49/month + ChatGPT Plus $20/month = $61.44/month fully reimbursed. That's $737/year in pure savings on services you'd pay for anyway.

The catch: this list updates. The original launch list was Netflix/Spotify/ChatGPT/Apple One. Apple One was dropped, TradingView and Amazon Prime were added. Verify the current list on Bybit's help center article before assuming a specific subscription qualifies.

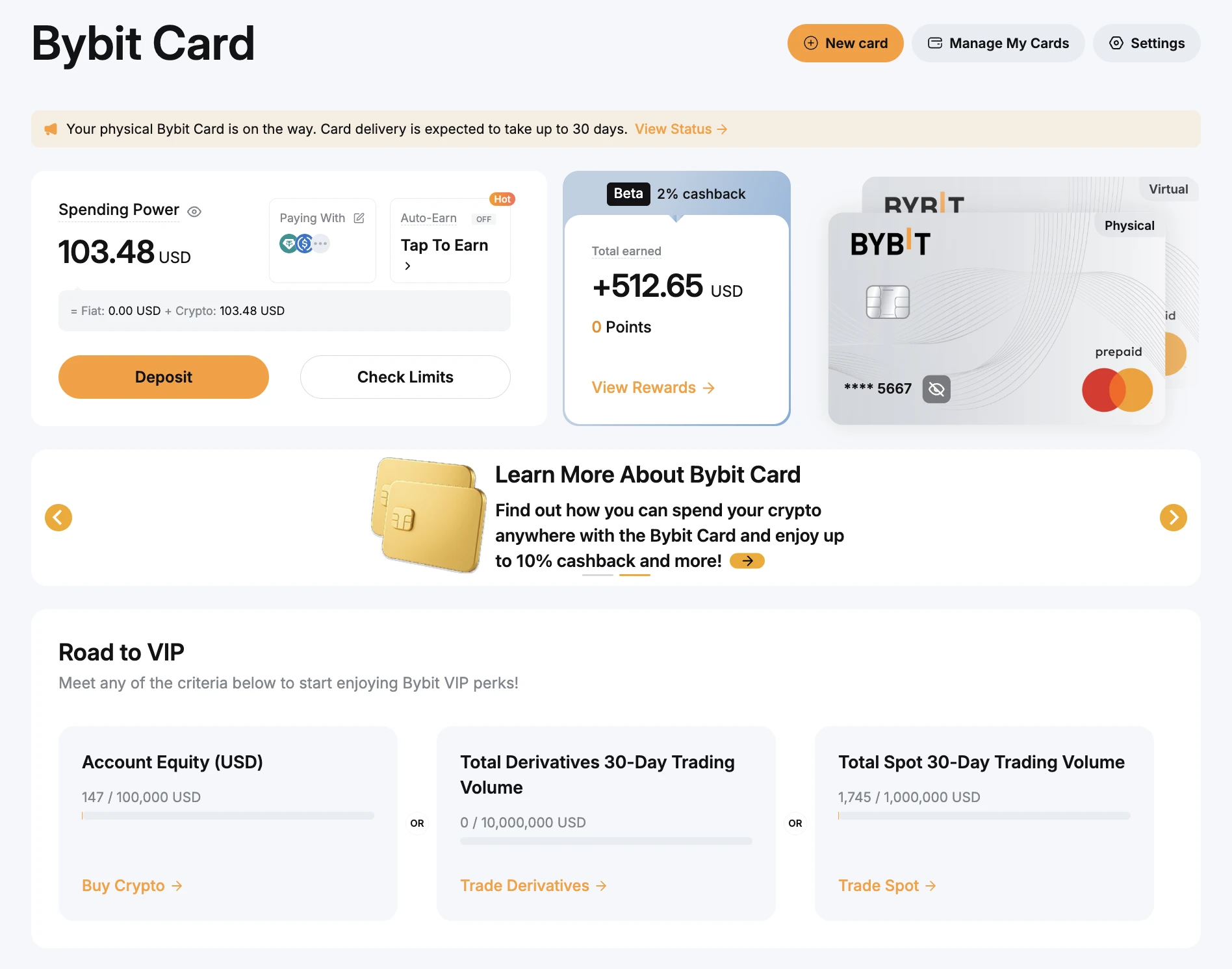

📱 Dashboard walkthrough — what you actually see in the app

The Card section in the Bybit app is structured around four areas:

- Spending Power — your available balance for card purchases, calculated from your Funding account holdings in supported assets (USDT, USDC, BTC, ETH, etc.). The dashboard shows your live spending capacity in USD.

- Pay With — which asset gets auto-selected for the next transaction. You can set a preference order (e.g., USDT first, then USDC, then BTC) — the system spends down in that order until balance runs out.

- Total Earned Cashback — cumulative USDT earned, with current tier (Beta 2% in screenshot example) and points balance.

- Road to VIP — your progress against the next tier criteria (Account Equity, 30-day derivatives volume, 30-day spot volume). Three parallel paths to upgrade tier.

The interface is clean — closer to Revolut / Wise UI density than the typical CEX clutter. Spending Power updates in real-time as your crypto balance changes.

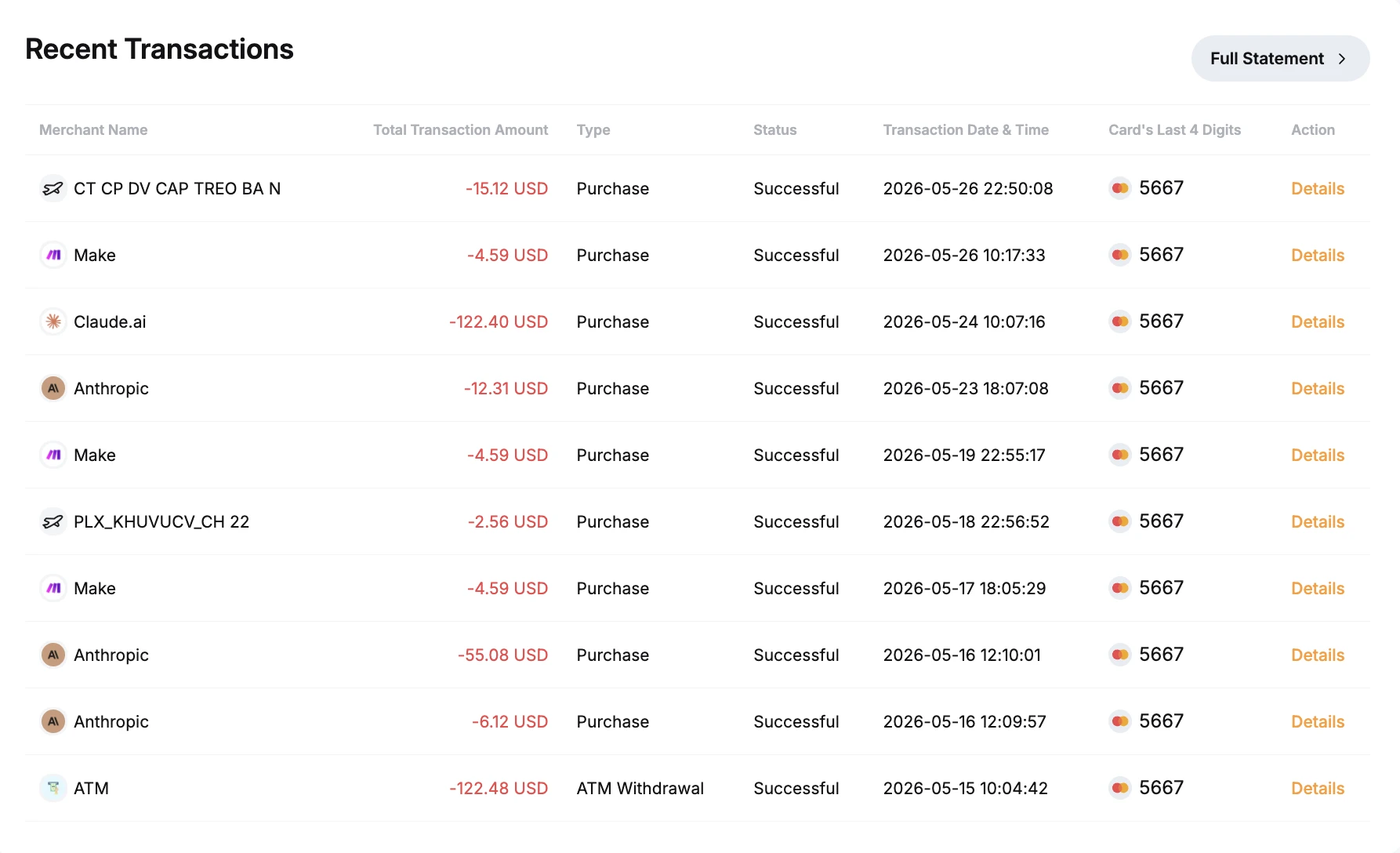

💸 Real transaction history — what the card actually pays for

The screenshot above is from an active card user (with sensitive amounts visible — these are real charges, not synthetic demo data). Visible transactions include:

- Anthropic (Claude API subscription) — $55.08, $12.31, $6.12

- Claude.ai (consumer subscription) — $122.42

- Make.com (automation platform) — $4.59 monthly recurring

- ATM withdrawal — $122.48

- Generic merchants ("CT CP DV CAP TREG BA N", "PLX_KHUVUCV_CH 22") — typical Mastercard merchant codes

What this shows in practice:

- Card works seamlessly for SaaS subscriptions (Anthropic, Claude, Make) — no failures, no FX surprises

- Works for ATM withdrawal — successful $122 cash withdrawal, fee structure visible separately

- Works at generic POS terminals — Mastercard merchant codes confirm regular acceptance

This is what daily usage looks like — not exotic crypto-payment scenarios, just paying for the same SaaS, subscriptions, and occasional cash you'd pay for with any bank card. The crypto-funding angle is invisible to the merchant.

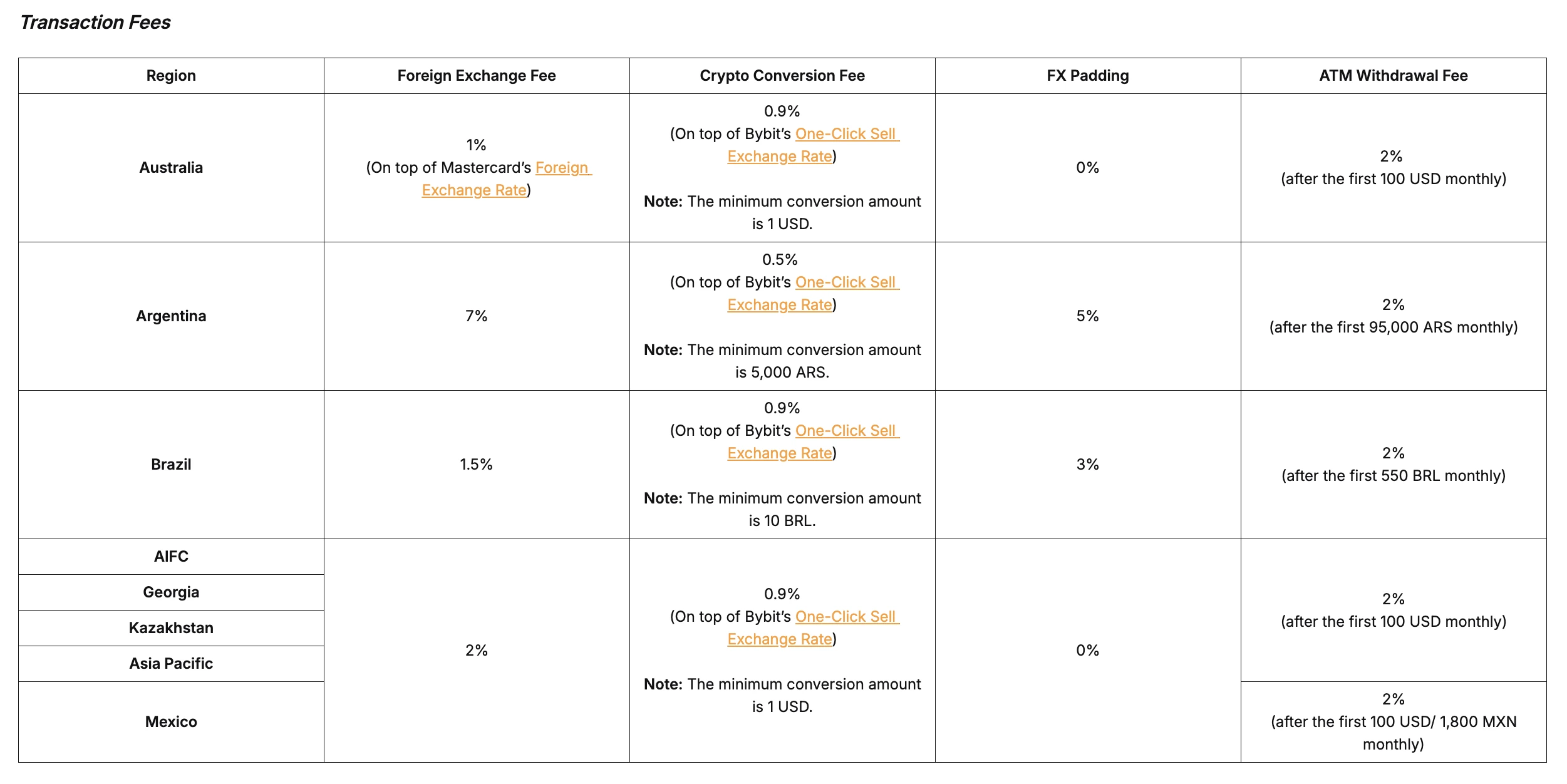

💰 Transaction fees by region — major variance worth knowing

This is where the math gets serious — fee structures differ dramatically by which region issued your card:

| Region | Foreign Exchange Fee | Crypto Conversion Fee | FX Padding | ATM Withdrawal Fee |

|---|---|---|---|---|

| Australia | 1% | 0.9% | 0% | 2% (after first $100/mo free) |

| Argentina | 7% | 0.5% | 5% | 2% (after first 95K ARS/mo free) |

| Brazil | 1.5% | 0.9% | 3% | 2% (after first 550 BRL/mo free) |

| AIFC / Georgia / Kazakhstan / Asia Pacific | 2% | 0.9% | 0% | 2% (after first $100/mo free) |

| Mexico | 2% | 0.9% | 0% | 2% (after first $100 or 1,800 MXN/mo) |

Breakdown what each fee means:

- FX Fee — applied on top of Mastercard's interbank exchange rate when transaction is in a different currency than your card

- Crypto Conversion Fee — applied when card converts your crypto to local fiat (sits on top of Bybit's One-Click Sell exchange rate)

- FX Padding — additional markup on the exchange rate applied in specific regions

- ATM Fee — for cash withdrawals at ATMs, applied only after monthly free quota

Practical interpretation:

- Best deal: Australia (1% FX, 0% padding) — total cost ~1.9% on a foreign transaction

- Standard: AIFC/Asia Pacific/Mexico — 2% FX, 0% padding, total ~2.9%

- Worst deal: Argentina — 7% + 5% padding + 0.5% conversion = ~12.5% total cost on foreign transactions. At 2% Base tier cashback this means you're net paying 10.5% extra for the privilege of spending crypto. P2P-and-spend is usually cheaper in this region.

If you live in a high-fee region (Argentina specifically), do the math first: is the convenience worth 10%+ extra cost vs traditional P2P-to-bank-to-card flow?

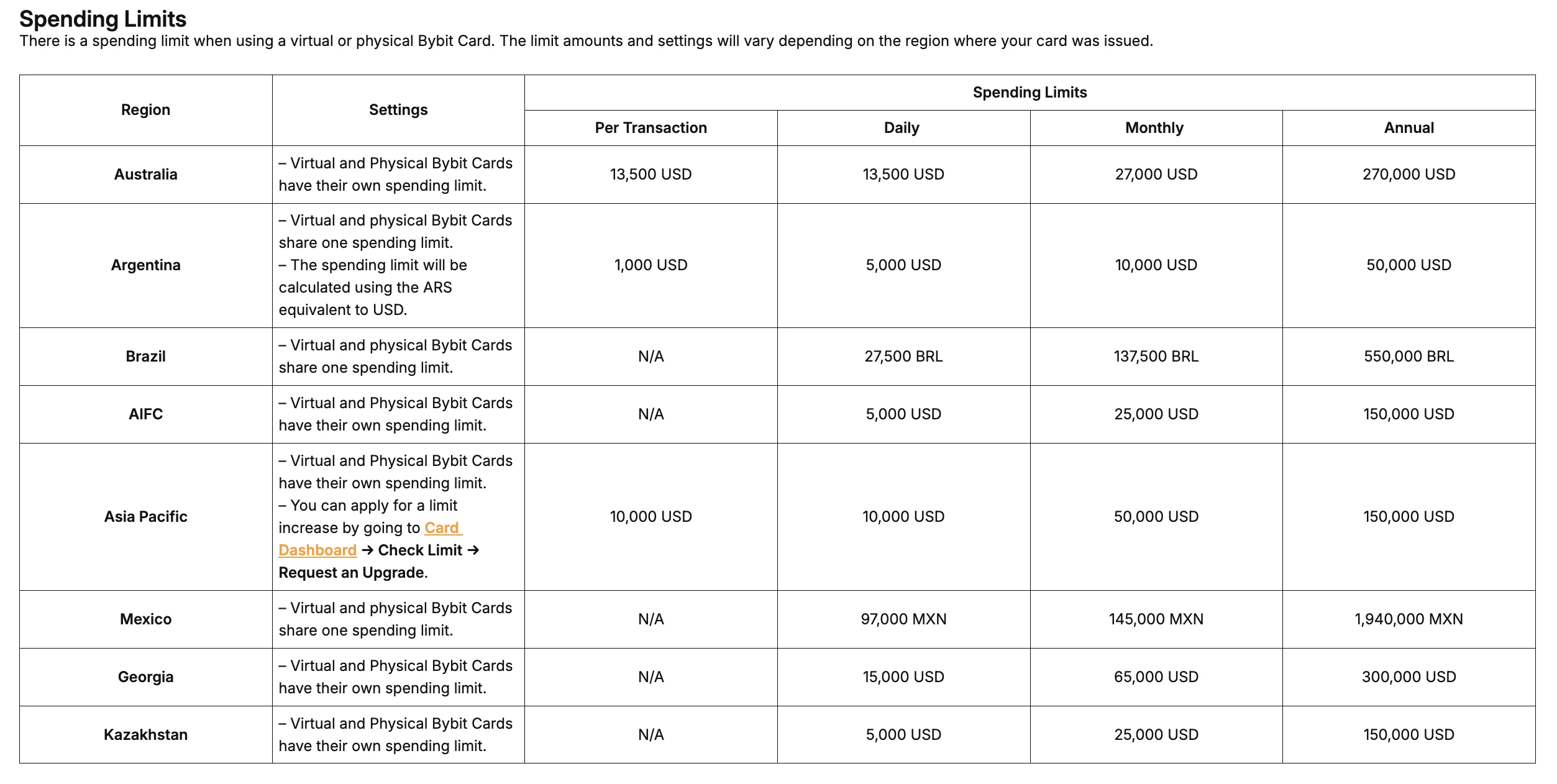

📊 Spending limits by region — how much you can actually spend

Spending limits are region-specific and split between Virtual and Physical cards:

| Region | Per Transaction | Daily | Monthly | Annual |

|---|---|---|---|---|

| Australia | $13,500 | $13,500 | $27,000 | $270,000 |

| Argentina | $1,000 | $5,000 | $10,000 | $50,000 |

| Brazil | N/A | 27,500 BRL | 137,500 BRL | 550,000 BRL |

| AIFC | N/A | $5,000 | $25,000 | $150,000 |

| Asia Pacific | $10,000 | $10,000 | $50,000 | $150,000 |

| Mexico | N/A | 97,000 MXN | 145,000 MXN | 1,940,000 MXN |

| Georgia | N/A | $15,000 | $65,000 | $300,000 |

| Kazakhstan | N/A | $5,000 | $25,000 | $150,000 |

Notes:

- Australia has by far the most generous limit structure ($270K annual)

- Argentina has the tightest limits ($50K annual) — combined with high FX fees, the card is positioned more for occasional use than primary spending in AR

- Asia Pacific (covering most SE Asian countries) sits in the middle — sufficient for normal retail use, may bind for high-spend users

- You can apply for limit increase by going to Card Dashboard → Check Limit → Request an Upgrade in Asia Pacific

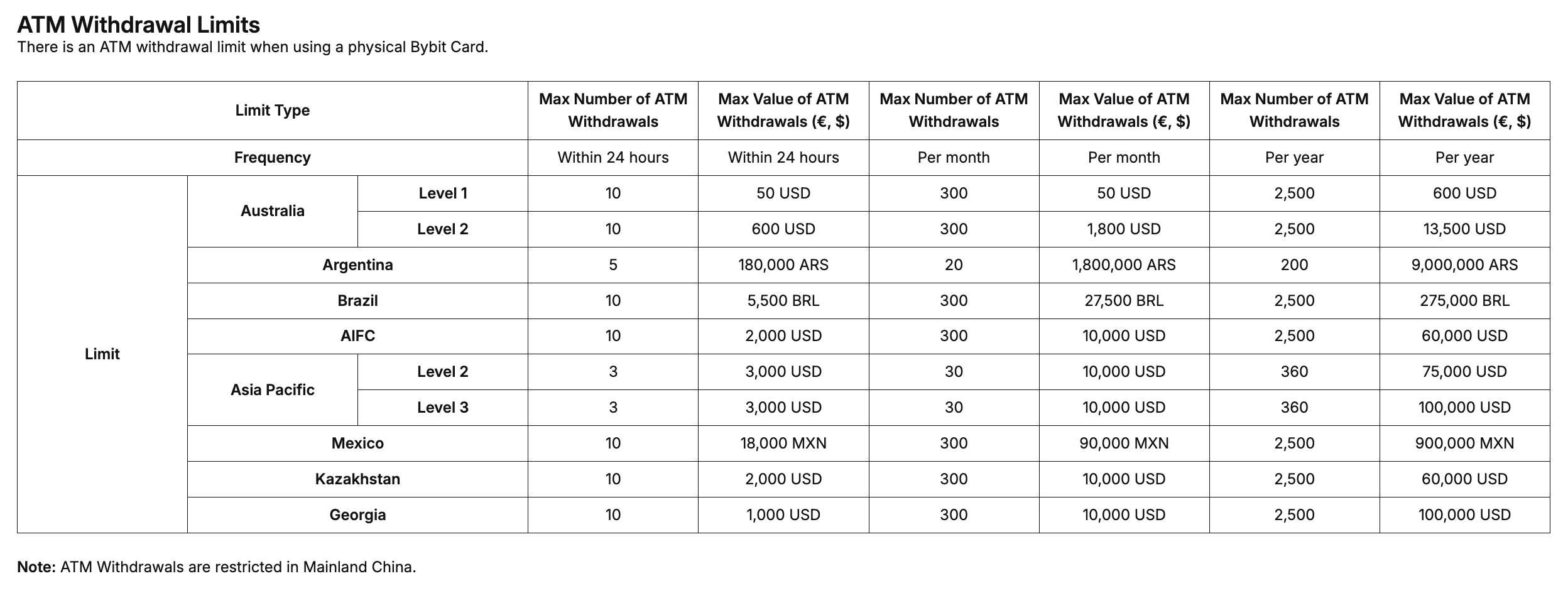

🏧 ATM withdrawal limits — cash access by region

ATM access is more restricted than spending. Highlights:

- Australia Level 1 — 10 withdrawals max within 24 hours, but capped at $50 USD per 24h

- Australia Level 2 — 10 withdrawals, $600 USD per 24h

- Asia Pacific Level 2 — 3 withdrawals, $3,000 per 24h

- Asia Pacific Level 3 — 3 withdrawals, $3,000 per 24h, $10,000 per month

- Argentina — 5 withdrawals, 180,000 ARS per 24h (~$180 USD equivalent)

Important: ATM withdrawals are restricted in Mainland China entirely. Other geos have specific carve-outs.

Practical implication: Bybit Card is not optimized as a cash-replacement card. If you frequently need physical cash, your daily ATM ceiling is meaningfully lower than what a regular debit card provides. Use the card for online and POS, withdraw cash from your local bank account.

⚙️ How to apply

The application flow takes ~10 minutes if your KYC is already at the right level:

- Bybit account — register if you don't have one, complete KYC Level 1 minimum (KYC Level 2 needed for full card features)

- Eligibility check — Bybit verifies your residency matches a supported region

- Card type — Virtual (instant, free) or Physical (~30 days delivery, may have shipping fee in some regions)

- Funding — deposit USDT, USDC, BTC, ETH or other supported assets to your Funding account

- Set preferences — auto-convert order, default currency for cashback, notifications

Once active, the card is immediately usable for online purchases. Add to Apple Pay or Google Pay for offline tap payments. Physical card needs activation via SMS or app confirmation when it arrives.

⚠️ Honest trade-offs

1. The 10% headline is unrealistic for most users. Real cashback for retail is 2% (Tier 1) or 4% (Tier 3 if you trade actively or spend $3.5K/month). Calibrate expectations.

2. Cashback is in USDT, not fiat. You earn cashback in USDT which sits on Bybit. To "spend" the cashback means putting it back through the card (which compounds), or selling to fiat (which costs you the same FX/conversion fees again).

3. Region FX fees vary wildly. Argentina at 12% total cost makes the card unsuitable for primary spending there. Run your specific region's math.

4. ATM limits are restrictive. Don't plan to use this as your main cash card — daily limits are 5-30x lower than typical bank debit cards.

5. Geo-restricted from US. Hard block, no workaround.

6. KYC required for full functionality. Level 2 minimum for most card features. Plan for the verification step.

7. Custodial exposure on Bybit balance. Your card pulls from your Bybit Funding account — any catastrophic exchange event affects card balance too. Don't keep more than monthly card float on the exchange.

🎯 Who Bybit Card is for?

| Profile | Verdict |

|---|---|

| Active Bybit trader (VIP 3+) | Strong fit — unlocks Alpha tier 4% automatically |

| Heavy SaaS user (Netflix + Spotify + ChatGPT + TradingView) | Strong fit — 100% cashback on the right list of services |

| EU / Australia / Asia Pacific resident | Good fit — favorable fee structure, decent spending limits |

| Casual user, low monthly spend | OK — Tier 1 Base 2% is fine but the card is not life-changing |

| Argentina resident | Skip — 12% total FX cost negates the cashback math |

| US person | Skip — geo-restricted |

| Need primary cash card | Skip — ATM limits too tight |

| Already using Crypto.com Card | Compare both — Crypto.com is more mature; Bybit Card has better subscription cashback list |

💡 Verdict

Bybit Card in 2026 is the strongest crypto card for users who fit a specific profile: live in a supported low-fee region, already trade on Bybit at VIP 3+, and spend monthly on the right 5 subscriptions (Netflix / Spotify / ChatGPT / Amazon Prime / TradingView). For that user, the math compounds — 4% baseline cashback on regular spend plus effectively free subscriptions equals 5-7% effective return on monthly card usage, which is genuinely market-leading.

For users outside that profile, the value is more modest. 2% cashback on a base tier in a 2% FX region nets you ~0% on foreign transactions — useful but not differentiating from any decent bank card.

The honest version: this is a great second card if you're already in the Bybit ecosystem, a marginal primary card if you're not.

💳 Apply for Bybit Card with welcome bonuses — affiliate disclosure above.

📺 Full video walkthrough on YouTube

📚 Official Bybit Card resources:

- Bybit Card guide on Bybit Learn — official introduction and benefits overview

- Fees and Spending Limits — full live fee schedule and limits

📚 Related articles:

- Crypto cards 2026 full comparison — Bybit Card vs OKX Card vs LinkPay vs SkyPay vs Bitmart

- Bybit security checklist 2026 — required reading before sizing up your Bybit balance

- How to deposit on Bybit in 2026 — funding your account before applying for the card

Register via my link

Apply for Bybit Card via my partner linkFrequently asked

Is 10% cashback on Bybit Card realistic, or marketing?+

The 10% rate is real but requires Tier 6 Infinite status, which means either Bybit VIP Supreme tier or $25,000 monthly card spend. For 95% of retail users that's out of reach — practical cashback for the typical user is 2% (Tier 1 Base) or 4% (Tier 3 Alpha if you hit $3,500 monthly spend or VIP-3 trading volume). The 8% Tier 5 Omega rate is achievable for active Bybit traders or high-spend users. Don't size the value of the card around the 10% headline — calibrate around 2-4% which is what you'll actually earn.

Which subscriptions get 100% cashback, and what's the catch?+

Five subscriptions get 100% cashback: Netflix, Spotify, ChatGPT (OpenAI), Amazon Prime, and TradingView. The catch is two-fold. First — there's a monthly cap on cashback pegged to your tier (Base 5 USDT max per month, Beta 50, Alpha 150, Apex 250, Omega 400, Infinite 600). If your subscriptions total more than the cap, only the portion within cap gets 100%. Second — TradingView is a recent addition; the original list was Netflix/Spotify/ChatGPT/Apple One, so verify the live list on Bybit's site before counting on a specific subscription. For most retail users spending $30-50/month on these services, the 100% cashback covers it entirely within tier caps.

Why do FX fees differ so dramatically between countries?+

Bybit Card has region-specific issuance and partner banks per market, and each region has different local payment infrastructure costs. Australia gets the best deal (1% FX, 0% padding). Asia Pacific / AIFC / Georgia / Kazakhstan / Mexico land at 2% FX with 0% padding. Argentina is the worst (7% FX + 5% padding = 12% on top of Mastercard's interbank rate). Brazil sits in between at 1.5% + 3% padding. If you live in a high-fee region, the cashback math has to beat your FX cost — at Tier 1 Base 2% cashback in Argentina, you're actually paying net 10% to use crypto on the card, which is worse than P2P sell-and-spend for most cases.

What's the difference between Virtual and Physical Bybit Card?+

Virtual Card is issued instantly in your Bybit app and works for online purchases, Apple Pay, and Google Pay. Physical Card is a real Mastercard mailed to your address (~30 days delivery), works at offline terminals and ATMs in addition to online. Both share the same spending limits in most regions, both earn cashback identically. Recommendation — start with Virtual (free to issue, instant), upgrade to Physical only if you need ATM access or specifically want a physical card for travel. Some regions (like Argentina) have separate Virtual and Physical limit pools, but most regions share one limit.

Can US persons get a Bybit Card?+

No. Bybit Card is geo-restricted from US users. Supported regions as of 2026 include Australia, Argentina, Brazil, AIFC (Astana International Financial Centre, Kazakhstan), Asia Pacific (specific countries), Mexico, Georgia, Kazakhstan, and parts of Europe. US persons are blocked from the card product entirely. If you're a US person — Coinbase Card, Crypto.com Card USD, or Gemini Card are the closest alternatives, with their own pros and cons covered separately.

How fast does the cashback hit my account, and in what currency?+

Cashback is credited in USDT to your Bybit funding account, typically within 24 hours of the transaction settlement (which is itself 1-3 business days after the swipe). Cashback shows in your Card → Rewards dashboard immediately as 'pending' and converts to 'available' once the original transaction settles. The 100% subscription cashback works the same way — your subscription charges through, then USDT cashback lands within ~3 days. Cashback can be withdrawn or used to fund future card spend immediately upon hitting 'available' status.

What happens if my crypto balance is too low at the moment of payment?+

The transaction is declined at the terminal — Bybit Card doesn't extend credit. You need sufficient balance in supported assets (USDT, USDC, BTC, ETH and others depending on region) in your Funding account at the moment of swipe. The card auto-selects which asset to convert based on your preference order set in Card → Settings → Auto-Convert. Pro tip: keep at least 1.5x your typical transaction size in USDT to avoid declines from price slippage during conversion, especially for non-USDT assets that need a swap step before fiat conversion.

Want a review like this for your project?

YouTube review + Telegram + an evergreen blog article — EN · ES · RU-CIS markets. Real audience, verifiable results.

Read next

✈️ AviaWallet Review 2026 — the Web3 super-wallet with a premium marketplace, auctions and travel in one app

🏦 Nexo Review 2026 — Borrow Against Your Bitcoin Instead of Selling It (Credit Line from 2.9%, ZiC 0% APR)